TO THE POINT: A tax-efficient retirement funding supplement

- Smart Money

- Dec 6, 2023

- 1 min read

THE SCENARIO

A successful couple (ages 45 and 43) are fast approaching retirement. Together, their household income is approximately $400,000/year. They have taken full advantage of their qualified plan opportunities, making the maximum contributions allowed by the IRS. After a recent review of their retirement plan, however, they decide that they need to contribute more toward their retirement. What are their options?

THE PROBLEM

The couple is in a high-income tax bracket now and anticipate remaining in a high bracket throughout retirement. With qualified plans off the table, they want to know if there are alternative accumulation options available to them – with tax advantages.

THE PLAN

Since the couple has a long horizon (10+ years), they are in good health, and they have an excellent positive cashflow, they may consider the following option:

Purchase an accumulation-focused, permanent, life insurance policy on one (typically the healthiest/youngest) or both of the individuals.

Policy is funded and set up to have the tax profile of a Roth account:

Premiums are paid with after-tax dollars.

Accumulation within the policy is tax-deferred. No increase in couple’s current tax liability, unlike typical taxable investments.

Policy distributions are set up to be received tax-free, further keeping their tax liability down during retirement.

The policy’s death benefit is received tax-free.

THE DESIGN

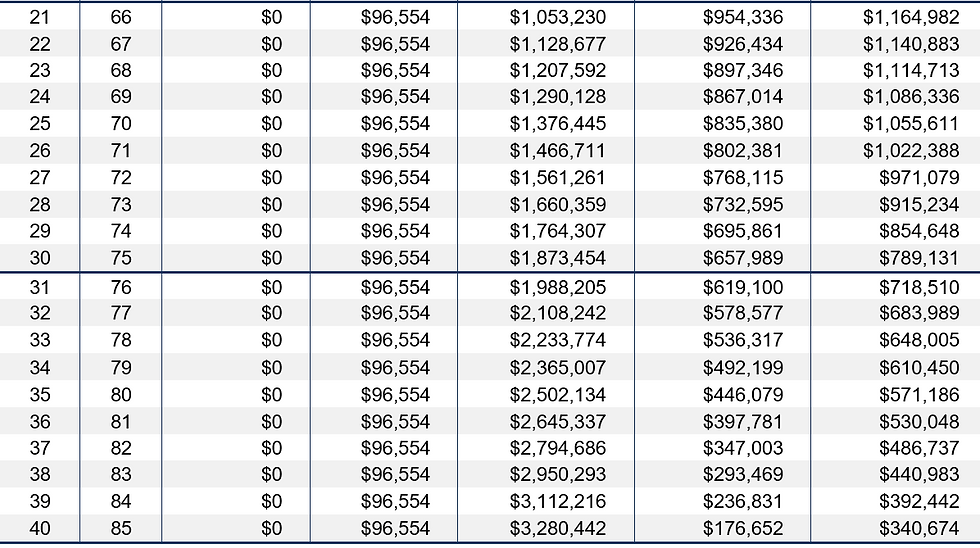

THE NUMBERS

The table, below, contains actual illustration amounts for a typical permanent product provided by a leading life insurance carrier. Your numbers will, of course, be different.

Sample: Male, 45, Preferred Non-Tobacco Initial Death Benefit: $399,880

Download the PDF:

Comments